Investing in "The Next Derivative"

Investing in "The Next Derivative"

Introduction

“We try to think about two things….things that are important and things that are knowable.”

- Warren Buffet, 1998 Berkshire Hathaway AGM

What do you make out of the following statements:

Among the greatest beneficiary of the US-China trade tensions would be a lesser-known Dutch company

A less windy year in Germany in 2021 caused a spike in North American Natural Gas prices even before the Russian invasion of Ukraine

One of the biggest beneficiaries of the European energy crisis would be fertilizer manufacturers in North America and aluminum manufacturers in the Middle East

African Swine Flu in China led to a sharp rise in Skimmed Milk Powder prices across the world

In all the above instances, the first part (the cause ) was easily observable, but its relation to the latter (effect) would be considered far-fetched or co-incidental to most. However, if I lay out the chain of “Cause and Effect” for each instance (which I will), it will be amply clear that these effects were “knowable” and “important”. And obviously quite profitable to the ones who figured it out before others. This is what we call investing in the “The Next Derivative”

First Derivative is a trap

Stock prices change every day and every minute of every day due to changes in our environment and the perception/reaction of traders/investors to those changes. Our brains are hard-wired to the “Cause-Effect” framework. I term the shortest and the most certain chain of “Cause-Effect” to be the “First Derivative”. Examples could be:

A rise in crude oil (copper, lumber, or steel ) prices leads to a rise in stock prices of the producer of the commodity

Rising interest rates are bad for growth stocks

Higher natural rubber prices are bad for tire manufacturers

All these are examples of first-derivative thinking and we would have a natural tendency to trade on these intuitive relationships. This is very alluring because:

The relation can easily be established by viewing two data points over time (two-time series data)

Easy to discover, explain and measure

Very reliable

Can be automated and scaled using computers

However, very soon one would realize that the approach is fraught with the following challenges:

Since it’s so obvious, everyone knows and understands it, and has probably traded it

The time gap between cause and effect is so less, almost instantaneous, the market just becomes reactionary. It often provides very little time to react

Extremely difficult for humans/individuals to beat computer programs to capitalize on such trades

Since the reaction is fast, we are not in a position to evaluate the scale of impact, leading to market over/under-shooting. This eventually leads to buying near the top and selling close to the bottom

In these markets, it is extremely difficult to have an information advantage ( except if you have insider information, which would make it illegal if you get caught ). The only sustainable advantage one can possess is “Analytical Advantage”

This is the reason I argue that we should look at second, third…..Nth order impact to gain an advantage over the average investor. This is the “Analytical Advantage” we gain by being able to decipher what the next derivative or the next chain of cause-effect is, which the market is still not pricing in. This is the advantage of “The Next Derivative”

Let us expand on the examples mentioned earlier to establish how “The Next Derivative” thinking is possible and profitable:

Among the greatest beneficiary of the US-China trade tensions would be a lesser-known Dutch company

We have all heard, read, and even suffered from the shortage of semiconductor chips that power all modern equipment, from cars to mobile phones, laptops, and even fighter jets and drones over the past couple of years. Most of the advanced chips (lower than 10-nanometer nodes), the ones that power your iPhones and Galaxy devices, are manufactured by just two companies, Samsung and TSMC. TSMC is the market leader by far and has all its manufacturing in Taiwan. As the chip prices rose, the first derivative thinking would buy all the chip manufacturers and designers (Qualcomm, Intel, NVIDIA, and AMD). However, it was clear that such a massive scale of chip shortage would lead to a matching expansion in capacity.

Besides that, such a large concentration of chip production in so close proximity to China makes the US and its allies nervous. This means we would see excess capacity and redundancy being created to geographically diversify manufacturing capacity and also avoid the supply chain nightmare we saw in 2020/21.

Semiconductor manufacturing is extremely capital-intensive and cyclical. Hence it was evident that massive redundancies built in by players would lead to lower profitability in the future, but the capacity would nevertheless be built. One of the most important components of high-end chip-making is Extreme Ultra Violet (EUV) machines. And there is just one Dutch company on earth by the name of ASML that has perfected the technology over decades. Even if the semiconductor industry was saddled with overcapacity for the next several years, the order book for ASML was full for the better part of the decade, and it was limited by its own capacity to produce and deliver. The following chart shows the relative price performance of ASML vs other players in the value chain from 2019 till Sep 2021 before the crash.

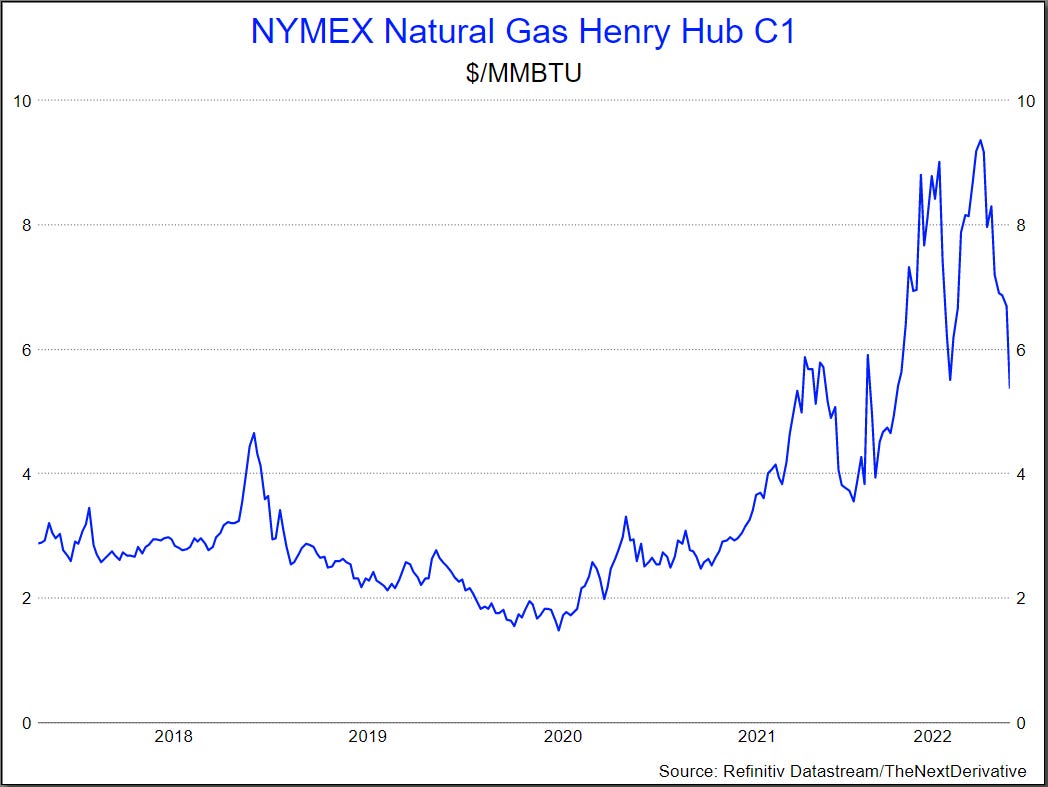

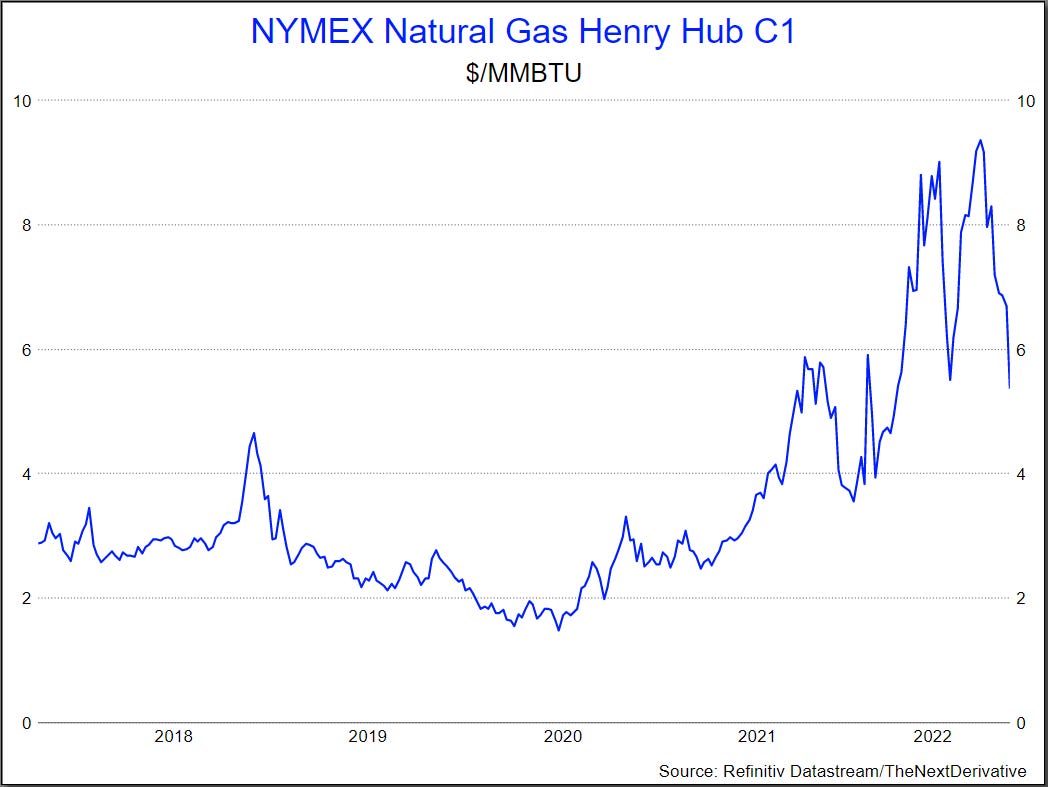

A less windy year in Germany in 2021 caused a spike in North American Natural Gas prices even before the Russian invasion of Ukraine.

Germany has over the past decade drifted significantly toward the renewable source of energy, especially wind. But the problem with the wind is, it does not blow all the time. 2021 was particularly a year with much less wind. This meant that there was not enough electricity generation which had to be compensated by power generation from Natural Gas. In addition to that, carbon credits prices skyrocketed in Europe. Since coal emits much more CO2 and coal plants had to purchase offsetting carbon credits at a higher cost, shifting from coal to gas was a viable option. This was depleting the natural gas storage in Europe which meant they had to procure LNG from global markets. Now US was the only country with excess capacity to export Natural Gas in LNG form, hence as LNG markets tightened Natural Gas prices in the US and Canada strengthened to the benefit of Natural Gas producers in North America

One of the biggest beneficiaries of the European energy crisis would be fertilizer manufacturers in North America and Aluminium Manufacturers in the Middle East

We all know that the sour relationship with Russia has led to the energy crisis in Europe. The shortage of Natural Gas (NG) in the EU is well established, with NG in EU trading at ~$44/MMBTU compared to just $5.8 in the US for Nov. The prices however cannot converge as there is not enough capacity to transport the gas (LNG Terminals and re-gasification capacities). What this meant is all the industries that require a massive amount of NG shut down in the EU. The prime candidate for that was fertilizer, especially Urea, where NG would form 70-80% of the total cost. Several leading fertilizer plants in the EU got shut, thus leaving the market for NA-based fertilizer companies to capitalize on as they have the largest and cheapest available gas to produce fertilizer. Since Russia and Ukraine were also among the largest grains exporter, the war lead to a sharp rally in grain prices, which increased the affordability of farmers, especially in NA to buy fertilizers at higher prices.

Similarly, Aluminium production is extremely power intensive and polluting. Due to massive pollution, China curtailed smelting operations, and plants in the EU had to shut down due to a shortage of energy. Thus giving Middle East based Aluminium manufacturers a field day

Or African Swine Flu in China led to a sharp rise in Skimmed Milk Powder prices across the world

This was the most unexpected one for me. China suffered a massive outbreak of the African Swine Flu in 2018 and 2019. This was being spread from infected to other animals as the smaller farms used the swine blood as feed for their herd. China immediately banned the practice, however, this led to a shortage of feed. Parallelly in the EU, due to its minimum support prices over the past 3 years had accumulated a massive stock of Skimmed Milk Powder (SMP). It could not sell in the market as it would crush the spot prices. The high stock of SMP was a massive drag on the entire Milk solids spectrum, and the SMP stock was getting close to the end of its shelf life. Now SMP can also be used for feed. China within a couple of months bought the entire stock of SMP for replacing blood-based feed for its swine herd, which it needed to rebuild. This removed the overhang in milk prices and led to the subsequent strengthening of the SMP and other milk product prices.

Why the next derivative is difficult?

Finding and correctly predicting the next derivative is profitable, but difficult. Or should I say, it is profitable because it is difficult. It requires an elaborate understanding of how different industries work together and where the constraints lie. Who would wield greater pricing power in the supply chain?

We cannot depend on past experiences because there will hardly be many past instances with an exactly similar chain of events. And if there are, the trades would get crowded again, and we need to move on to the next derivative

As we move down the cause-effect chain to seek profitable trades, the number of possible outcomes keeps increasing, and the probability attached to each event in each path decreases (think of a probability tree). It demands greater knowledge and a stronger conviction to make a bet.

And the most important part is, we should know when we have gone too far. At the beginning of my career, I read a research report by a reputable analyst on a jewelry exporter from India. One of his central arguments was that due to global warming, the number of hurricanes in the US is increasing. This has made/would make US citizens more God-fearing and they would purchase more Golden Cross and chains to wear around their necks, thus benefitting the company. It appeared quite far-fetched to me, but I know how embarrassingly close I have been to similarly far-fetched ideas. I am sure I heard it in one of the Marvel movies that

“The most important thing about having a power is knowing its limitations.”

Knowing the limitations of one’s ability to reliably predict the future down the next derivative cannot be overstated.

Over a career spanning 15 years, I have worked to build a latticework of knowledge that has helped me connect the dots, know what others consider unknowable, and capitalize on what others think is unimportant. In my articles and posts here, I intend to share my learnings and use them as tools to untangle the tricky knots of the current markets. Do consider subscribing and sharing the word if you find my work interesting.