Should Indians Invest in Global Equities?

Should Indians Invest in Global Equities?

Benefits of adding Global Equities to Indian Portfolio

India has been great….

India’s NIFTY 50’s performance over the past decade has been far superior to diversified global portfolios leaving other emerging market indices and ETFs in the dust. Despite having a more traditional and diverse exposure vis-a-vis the growth and tech-focussed NASDAQ Composite, their performance has been similar after the recent meltdown in US growth equities.

The outperformance in the past two years has been an even greater revelation.

However, most of that decade of outperformance sheen comes off once we take into consideration the INR depreciation. The chart below shows the relative performance of NIFTY 50 in USD.

Though the performance is still higher than World and EM markets, they are significantly lower than the US indices.

As an Indian investor, one can argue that most of their expenses and liabilities are denominated in INR, so why should they be bothered by USD-denominated performance? To some extent that is true; however, having some USD-denominated asset could have provided a hedge against that currency depreciation, and ignoring such options, in my opinion, is an opportunity foregone.

With that anecdote, let us dive into reasons why Indians should consider including Global Equities in their portfolios.

Why Consider Investing Globally

Sector / Theme Exposure

I started my career in Indian equities in 2007 when BRIC theme still had some legs.

[ Goldman Sachs released one of the most popular research papers in 2001 titled “Build Better Global Economic BRICs” giving birth to the acronym BRIC, which meant Brazil Russia India China]. One of the key selling attributes of India compared to other members of the BRIC countries was the diversification Indian markets offered. That remains true to date. India remains a diversified market and a much-diversified economy today as can be seen in the chart below.

It is true that we have excellent companies in varied sectors, however, there are some sectors/industries or parts of the value chain that are completely absent or inferior in growth/resilience parameters. Let us look at some examples:

Social Media and Big Tech - This is the easiest and least contested one. India does not have its version of Meta (Facebook), Twitter, or Snap. If you wanted to get exposure to the growth of Social Media globally, we had to look at US markets. Similarly, Google, Apple, and Microsoft, three companies that I think have the largest and most defensible moats are also listed in the US. There is no company comparable to them in India or anywhere else. The most worthy competitor to Apple is Samsung, which is can be accessed through its London-listed GDR. We can throw in the audience's favorite Tesla in there as well. For cyber security, companies like Cloudfare, CloudStrike and Palo Alto Networks are also listed in US only

Ecommerce and shared economy- India in the past decade has produced several players in this space. However, they are at different stages of the lifecycle. As a portfolio manager (even for a personal portfolio), you would want to have exposure to companies at different stages of their lifecycle. This is an industry with a high mortality rate and the winner often takes it all. It makes sense to have sufficiently large global players who have achieved the scale. The “prime” example is Amazon, followed by Uber and Netflix.

Other Themes - Besides the obvious ones mentioned above, there are several other themes for which we do not have listed companies in India to play them adequately. For example, the chip shortage of last few years. The chip designers like Qualcomm, NVIDIA, Intel are listed in US. The chip manufacturers (foundries) like Taiwan Semiconductor (TSM) have US-listed ADR, and Samsung Electronics is again listed in London.

If you wanted to play the energy scarcity in Europe, the best way to play them was through Energy Companies listed in the US. There are very few options to play energy exploration in India, and they are not in a position to capitalize on the opportunity.

Similarly, if you were bullish on precious metals, most of the Gold and Silver miners are listed in US and Canada. If you are like me and think Nuclear energy is the most promising way to solve Carbon Emissions, you would find most of the Uranium Miners listed in Canada and US. If you were bullish on Iron Ore prices, you might want to buy the most profitable and lowest-cost producer of high-grade Iron Ore miner by the name of Vale (Brazil), again listed as ADR in US.

Factor Hedging

Factor hedging might sound complex, but is simply taking exposure to hedge risks in your current portfolio. For example, if you are invested in a steel manufacturer in India, whose earnings are negatively impacted by the rise in Iron Ore prices internationally, you might want to seek investment in Vale. Similarly if Natural Gas is a large part of your cost ( like in Chemicals and fertilizers) you might want to hedge that by investing in Natural Gas producers in US / Canada.

India Growth Story

It is true that India currently is the fastest-growing large economy, however:

India is not the only fast-growing large economy. There are several other countries at different stages of development that have excellent growth prospects. Eg: Macardo Libre, hailed as Amazon of Brazil, is listed in US. Tencent, the company behind WeChat with the largest portfolio of online game titles has an ADR listing in US.

These global companies would also benefit immensely from India’s growth. The largest user base of Facebook is India (~350 mn), and the Average Revenue Per User (ARPU) of FB from India is ~$4.5, while that from US is $49. As digital advertising gains in India, the benefits would flow directly to companies like FB and Google. As more cloud adoption happens in India, it would benefit companies like Amazon (AWS) and Microsoft (AZURE).

Valuation Gaps

The headline valuation of Indian equities appears to be slightly overvalued compared to S&P500, however, once you dig deeper into the composition of the market and specific stocks, the valuation would appear to be exorbitant, despite whatever growth the company is clocking. Just digging one step deeper, I gathered median PE for all the GICS Industry groups in India with a Market Cap of over $200mn. Since the last year's earnings might have been disrupted by COVID, I took the Max EPS over the past 3 years and the current price to compute PE at the company level.

We can see above that a few sectors that are either not best evaluated on PE (like Banks), cyclical industries (like Metals and Mining), or low growth sectors like Utilities have significantly low PE, but reasonable MCap. If we remove these sectors, PE ratio for the market goes even beyond Wt. Avg of 24.2x.

Taking a closer look at the most renowned names in the market, we see how high the valuations are and not adequate growth in EPS to support them.

I know that the past does not necessarily represent the future, however, the difference in the growth that is priced into these companies vs what they have exhibited in the past 5 yrs is extremely high.

Another example can be seen from the relative valuation of Nestle India vs Nestle Global.

Nestle Global trades at ~18x earnings while Nestle India traded at ~91x. The funny part is, Nestle Global has better growth than Nestle India because it pulls in growth and earnings from all the countries, including developing ones where the penetration of baby products is far lower than India.

If you contrast these companies with global leaders who have much more valuable IP and a global market to cater to, trading at similar or much less valuations, it would further underline the need to have some measured exposure to other global markets. Below is a list of a few leading companies from the US for comparison. And none of them are confined to US soil for their business.

Why the over-valuation?

India is among the very few countries which have a long-term growth prospect intact and there have been several major structural changes in the economy feeding the optimism. In other words, some of this valuation might and would play out in the medium to long term through earnings catch-up. However, one of the reasons for such high valuations can be that India has become a “boxed trade” for domestic investors.

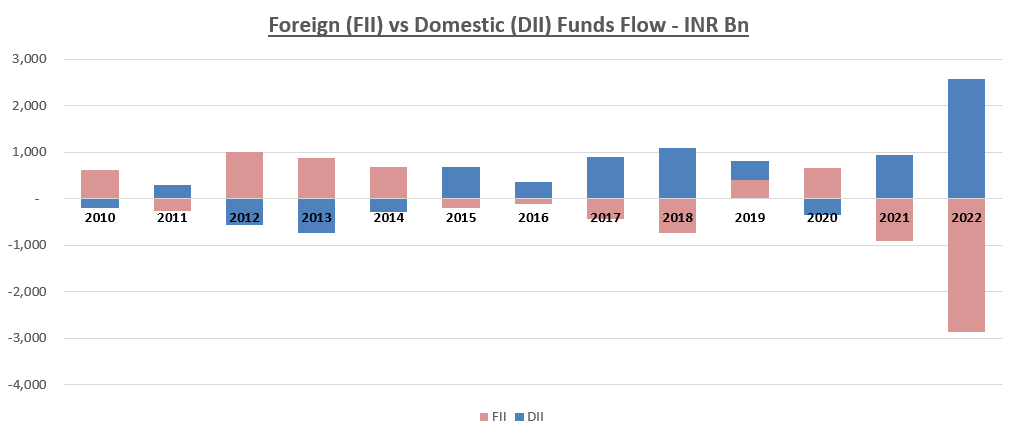

What I mean by that is, for decades Indian markets relied on foreign institutional capital (FII) to price the markets as domestic participation in Equity markets remained very low. But over the past decade, the participation of domestic investors through direct investing and through Mutual Funds has made FII much less relevant. As we can see in the chart below, FIIs have been net sellers in 6 out of 8 years after the landmark 2014 elections. But DII more than compensated for those outflows.

As of March 2022, the share of domestic investors (Retail, HNI, and DII) in NSE-listed companies went up to 23.3% (vs 18.5% in Mar 2015) compared to the FII share of 21.15% (vs 23.3% in Mar 2015). Interestingly, the share of retail investors was 7.42%, very close to that of DII at 7.75% (source).

The trend received a shot in the arm when Pension Funds were allowed to invest heavily in Equity markets post-2014, and pension participation was made open to non-government employees as well. This domestic fund was finding a home in Indian Equity markets and could not (or was not capable/willing) to invest abroad. When FII flows were relevant, they would exit India when they found better valuation elsewhere, thus keeping the valuations in check. However, for the tidal wave of domestic investors, their defined universe is India, as they go on to seek a “local maxima”. This, in my opinion, has made India a “boxed trade”.

As valuations continue to push higher as higher proportions of household wealth is moved from fixed assets (Gold, Real Estate) to equities, Rupee returns would follow, but would also trigger FII outflow thus depreciating Rupee and making Dollar returns tepid.