(When) Will META Pivot !!

(When) Will META Pivot !!

Margin of Safety in META - Evaluating the Resilience and Optionalities

“We posit that a value-based margin of safety is all too often used to justify ownership of dying businesses. While cheap, these value traps do not control their own destiny, devoting resources to life support and/or blind attempts at reinvention; and, all too often, it’s too late. Instead, the ability of a company to adapt – which, in turn, is dependent upon management Quality and nature of growth – is critical to any formulation of margin of safety.” - Redefining Margin of Safety, NZS Capital

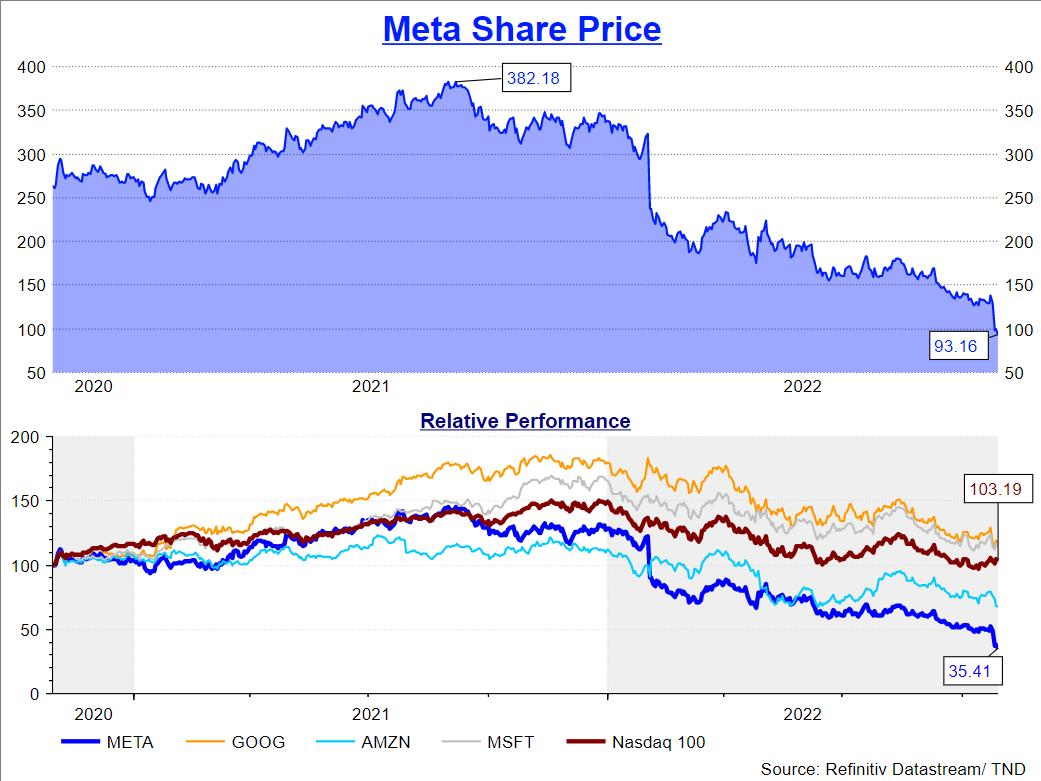

Meta released its Q3 2022 earnings on 26th Oct, and it saw its share price tumble 23% in a day. That is approximately $80 bn of Market Cap wiped in a day. Even before the recent fall, Meta lost 66% of its value from the high of $382 it saw in Aug 2021. Hence the underperformance of Meta was quite severe even before the recent crash.

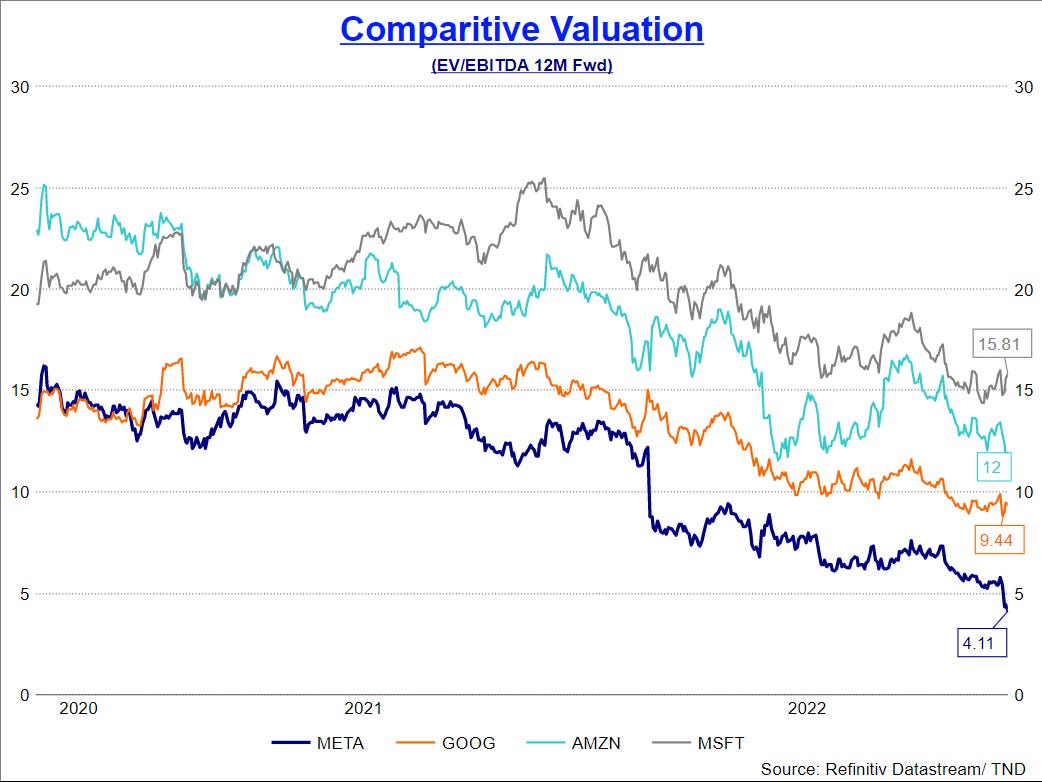

Though NASDAQ 100 is flat after 2 years, META has significantly underperformed its peers, both in terms of absolute share price (above) as well as the valuation, measured by EV/EBITDA as seen in the chart below:

This shows that the troubles in META (both absolute and relative) have not manifested themselves in this quarter’s earnings, but have been plaguing the company for a couple of years now. We will not discuss the Q3 results specifically in the article but refer back to sections of the release for context (An excellent review of the results can be found here posted by Stock Market Nerd, who I can’t recommend enough).

In this post, we will look at the “Resilience” and “Optionality” in Meta’s business, inspired by the excellent paper titled “Redefining Margin of Safety”, published by NZS Capital. In a nutshell, the paper argues that the Margin of Safety, as defined by Ben Graham and further popularised in the excellent book by Seth Klarman titled “Margin of Safety”, needs a refresher in the current day and age. Instead of looking at cheap valuation as a source of “Margin of Safety”, we should look at what is resilient in the business and the optionality it provides.

Resilience Of The Core

A modern network / platform-based company should be evaluated on 3 basic parameters. I will take this opportunity to also draw an analogy with railroad companies:

Reach and User Penetration - This is akin to railway tracks that railroad companies lay. Growing these tracks take a lot of investment but once they are built, they are very cheap to maintain. Companies do not generate profit on the length of tracks, but everything else runs on them. Once they reach a certain size (penetration), the focus should be on maintaining the reach, growth is secondary.

Engagement - This resembles the number of trains you can run on those tracks. the more traffic /engagement you get on your tracks/platform the more opportunities to get revenue. Just like tracks can run different kinds of rail cars, platforms can run different kinds of content (pictures, audio, video, etc.)

Monetization - This resembles how much a railroad company charges for the capacity that runs on its tracks. Just like the strength of the railway network and its operational superiority compared to alternative modes of transport determine how much fare/freight it can charge, similarly, the level and quality of engagement on a platform determines how well it can monetize the traffic on its network

Reach and User Penetration

Is Facebook, and its Family Of Apps (FOA) still relevant?

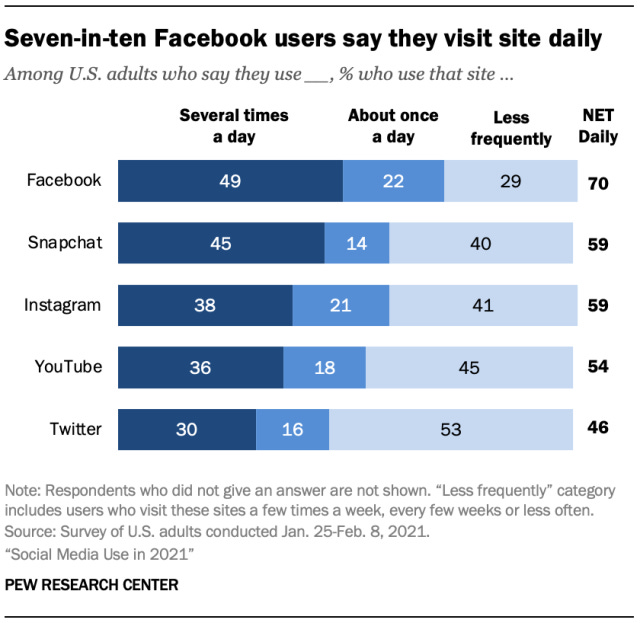

At its heart, Facebook as a platform and Meta as a company is a social network. Its strength lies in its ability to connect people and the size of the network. Despite all the bad press over the past couple of years, users have not abandoned the platform. In fact, it still keeps growing despite reaching saturation in a few markets.

Monthly Active People (MAP) (individuals) using any of its platforms stood at a massive 3.7bn (up 4% YoY) with 79% of that or 3bn people using at least one of the apps daily. Excluding the barely monetized Whatsapp with 2bn daily active users, Facebook’s (the app) Daily Active Users (DAU) stands at 1.9Bn growing by 2.8% YoY and 9% in the last 2 years.

This clearly shows that users ARE NOT abandoning the platform. Yes, the user growth is not as exponential, but at that scale and penetration, it is unreasonable to expect a much higher growth.

Though the penetration might seem high, suggesting limited growth, I feel demographics will support user growth going forward. Let me elaborate.

Facebook Users by Age Group (USA - Sep 2022)

Currently, only 22% of users are 55 years or older. It is however intuitive to expect that penetration at higher age brackets would be lower due to technology adoption challenges at older ages. As this 35-55 years demographic turns older and moves into the next bucket, as long as they are not abandoning the platform (which we saw earlier), the penetration at the higher age buckets would rise automatically. All Meta needs to do is keep the younger audiences enlisting going strong. This is essential for its long-term sustainability.

Engagement

Will TikTok kill FB / Instagram ? Is the social graph still valuable?

Short Form Video (SFV) has been a rage globally and TikTok has been at the front and center of this. Meta was indeed late to recognize the attractiveness of the market and introduced Reels late last year. But this is not something new. Meta is often quick to copy the success of other platforms to win back engagement, which has a much better ecosystem in the world’s largest social network. We saw this happening recently with Snapchat introducing Stories, which was then quickly adopted and integrated into Facebook and Instagram. And now Snapchat is not even in the race. Imitation is in the DNA of FB, and it’s not a bad thing. It has borrowed from MySpace, Orkut, and even the failed Google+, adding successful features to its platform. This shows off the resilience and adaptability of the business. We need to realize the source of Meta’s moat is not features, but the social graph. Besides offering a way to remain connected to friends and family, the social graph also ensures a ready audience for new and existing creators.

A key point that Zuckerberg stated in the call:

“And I do think that our somewhat unique mix of both having the kind of social friends and family content and the ability to drive recommendations, which I agree with some -- the premise of the question there, and that creators do want their content to be on multiple platforms, which I think is a little bit different from friends content where you want to, for the most part, share where your friends are, and you're not trying to have it be everywhere.”

Therefore, for social content, Meta’s platform remains the sticky choice, but it does not stop the creator-driven content to be hosted and shared there as well.

If Reels is able to provide tools for creators (which it is rapidly doing), there is no incentive for a creator to restrict itself to TikTok or Youtube Shorts.

However, this might be a symptom of a larger disease. As discovery and recommended content is getting more popular - like in TikTok, and now 50% of the content in Meta’s feed is recommended (viz content from accounts you do not follow), does this mean the advantage of the social graph is weakening? If this happens to be true, then the moat of Meta is significantly compromised in the longer term. However, we have no conclusive evidence of that as of now.

Monetization and Profitability

Has iOS’s ATT killed Meta?

iOS 14.5, fully rolled out in 3Q2022 changed structurally how Meta and all ad-supported platforms run and monetize (watch this for an explanation). App Transparency Tracker (ATT) limits the ability of Meta (and similar apps) to target and measure ads in a deterministic way for iOS users who opt out of tracking. Meta early on said that it would result in $10 bn a year in lost revenue due to this. However, let’s look at the numbers.

Ad revenue for the company in Q3 2022 was down by 4%, but if we remove the forex impact of rising USD, it was actually up by 3%. But Meta was not the only one to face this. Even YouTube ad revenue was down by 2%. So the reason for slower growth (because Meta’s ad revenue in constant currency grew) was geography mix (growth coming in from lower-earning regions), severe macroeconomic headwinds, and sub-optimal Reels monetization (more on this later). Hence, we do not see a major headwind from ATT translating into actual numbers.

Though ATT has and will jeopardize the ability of Meta to target and measure ads, thus impacting ROAS for advertisers, there are two important points to consider.

Digital advertising is still far better than any other alternative. If you are running and winning an 800 m race, it does not matter if you win by 40 sec or 20 sec. The gap between digital advertising and traditional advertising is far bigger. So ATT has chipped away some differences, but not eradicated the lead of digital advertising

Meta is not the only one impacted. Within the digital ad universe, the only company that benefitted from ATT was Apple itself. But Apple does not have a social network platform like FB or Insta, or a cross-platform messaging service like Whatsapp used by 3 bn people every day.

Therefore, I do not see the allocation to digital media or to the Meta platform’s share of that allocation depleting. If ROAS does come down, the advertisers would have to bear that burden, not Meta.

On the contrary, Meta has the resources and ability to build probabilistic models (against deterministic ones that relied on the pre-ATT era) which most of the smaller players would not be in a position to develop given the massive scale of investments required in AI and internally generated data to feed that AI. So in the mid to long term, Meta might actually stand to benefit from this move.

We should also keep in mind that iPhone’s smartphone market share is only 16% globally (50% in the US). Industrywide, opt-in rates are actually at about 25% — up from 16% in May 2021. For gaming, the opt-in rate is up to 30%. Based on the Mobile App Trends 2022 report, data from AppLovin-owned studios shows multiple popular games yielding opt-in rates as high as 75%.

Can Meta monetize Reels effectively?

Reels being a newer format is not monetizing as well as feeds. This is resulting in close to $500 mn per quarter loss of revenue. However, it is essential for Meta to scale the business before dialing in ad load on this format.

There are now more than 140 billion Reels plays across Facebook and Instagram each day. That's a 50% increase from six months ago. Reels is incremental to time spent on our apps. The trends look good here, and we believe that we're gaining time spent share on competitors like TikTok.

- Mark Zuckerberg

We have seen this script before with Stories where it did not monetize as well initially but then came at par with feeds. Management expects this to be the case with Reels as well and expects the parity to come in 12-18 months.

Why is ARPP/ARPU declining? Will this continue to be a headwind?

The Average Revenue Per Person (ARPP) for FOA was lower by 8% YoY ($7.53 vs $8.18), while the Average Revenue Per User (ARPU) for FB was lower by 5.9% YoY ($9.41 vs $10). This was due to a mix of currency impact, 18% lower price per ad, and geography mix. Let’s linger on the last factor.

Asia Pacific (AP) has been one of the major user base growth sources for Meta. DAU in AP grew by 16.23% in the last 2 yrs compared to 9% worldwide. This has translated into AP’s share of DAU growing from 40% in Sep-20 to 42.5% in Sep-22. This is important because there is a massive difference in ARPU between regions.

The ARPU in US and Canada is 11x the ARPU in AP, the largest user base of FB. As these economies mature and digital advertisement gets a stronger foothold, there is a strong argument for AP ARPU to move directionally closer to US and Canada. Meta has laid the tracks, it just needs to run more trains on those tracks there. For every dollar of increase in ARPU in AP, Meta’s revenue grows by $1.3bn per quarter or $5.2 bn annually. In the short run, however, worldwide ARPU would continue to decline as more growth comes from lower-yielding regions. But we also need to keep in mind, unlike other SAAS companies, Meta has negligible customer acquisition cost.

Optionalities

In the above section, we have discussed the parts of the business which appear to be resilient and adaptable despite macro and company-specific headwinds. In this section, we discuss the optionalities built within Meta’s ecosystem.

Running More (and Different) Trains on the Tracks

As discussed earlier, the user network is like a network of tracks. Once that is established, we just need to find more and different trains to run on them. A great example can be the WeChat of China. It started as an instant messaging platform reaching 811 mn users or 58% of the Chinese population. It then acted as a distribution channel for several other apps integrating food delivery, cab, ticket booking, grocery shopping, and several other use cases. With ~3bn DAU, Meta can and would try to do something similar:

Click-to-Message And Click-to-Whatsapp

Click-to-Message allows users to click on an ad and start interacting with the advertiser directly. This can lead to inquiry, support, and even sale. This is beneficial to users and advertisers for obvious reasons, but also has two major benefits for Meta.

It is a major differentiating factor compared to other platforms like TikTok or YouTube which do not have an integrated chat feature

It moves Meta ads even further down the funnel of the customer journey. Without this, ads are just impression ads that can be for lead generation. But with direct integration, Meta would get more credit for conversions, thus helping them get better ad rates.

It is already the fastest growing ad product with a $9bn annual run rate and comprised mostly of FB Messenger. Click-To-Whatsapp was introduced more recently and is already growing 80% YoY clocking a $1.5bn run rate. With over 2 bn daily active users, this has massive room to grow. Meta launched Jio Mart in India, an online end-to-end shopping experience, all built within Whatsapp (watch here ).

Paid Messaging

As Whatsapp and Messenger are among the most popular chat destination. And what better place for businesses to communicate with individual customers. This is the elevator pitch for Paid Messaging or Business Messaging. Through this, businesses can deploy their chatbots and customer support delivery to where the user is, i.e WhatsApp and Messenger. In its Conversations Event, Meta shared that over 1 bn users connected with businesses through its chat ecosystem. And earlier this year, Chat for Business was made open for businesses of all sizes. Imagine you can check your credit card transactions and balances from WhatsApp, or initiate a chat with technical support if your laptop is not working, or claim insurance through Whatsapp in case of an accident. Banks like ICICI Bank of India have already started this along with several other retail, e-commerce, and consumer goods companies.

Automated Advertising - Advantage+

As loss of signal through ATT became evident, it was clear that ad platforms could not depend on deterministic ad targeting and move to a more probabilistic ad targeting. In simpler words, traditionally advertisers would select filters and conditions like gender, location, recent purchase habits, age, etc to target their audience. However, with ATT many of these signals would become difficult for players like Meta and Google to get access to. Hence through automation, they would use Machine Learning and AI to decide which ads, in which format to show to which users. Think of the recommender systems used by Amazon or Netflix, but for ads.

As user interaction with such ads increases, the AI algorithm would learn from such behavior and further tune its algorithm to generate lower costs and better Return On Ad Spend (ROAS) for advertisers. Meta claims that such AI-driven automation has caused Cost Per Action (COA) to decrease by 12% and ROAS to increase by 15% in this short term for select customers. More details can be found here and here. A similar product was also launched by Google through its Search Ad Automation. Besides being a reaction to ATT, this also automates the process for advertisers making it easier to start for smaller businesses who do not have the resources or skill to effectively run ads on Meta platforms. This can help in increasing the penetration of digital marketing thus increasing the size of the pie as well.

Reality Labs and Metaverse

We can’t get away with discussing optionalities without discussing Reality Labs. This is an attempt by Meta to control the ecosystem and it is utilizing its might and cash flow to gain a lead on everyone else. This is a massive and costly bet and almost no one has a complete grasp on what it will pan out to be, but most would agree that the payout can be huge if Meta does succeed in owning and defining the ecosystem for the Metaverse. But we would need several more articles to discuss the opportunities and different scenarios in which it can play out. The progress though has been quite encouraging on the development front as we see several key players joining hands to contribute to the ecosystem:

“To deliver a great work and productivity experience, I'm excited about the partnerships we announced with Microsoft bringing their suite of productivity and enterprise management services to Quest, Adobe and Autodesk bringing their creative tools, Zoom bringing their communication platform, Accenture building solutions for enterprises, and more.”

- Mark Zuckerberg. Q3 2022 Earnings Call

I am quite optimistic about VR and AR use cases in retail, gaming, and as an alternative computing device (watch here, and here). Since the upside is enormous but unmeasurable, if Meta succeeds, we will discuss the near-term financial impact in the next section.

What spooked the markets?

Slower Revenue Growth

Meta’s revenue growth profile has been collapsing over the past few years. However, the flattening of revenues, 2% in constant currency terms, was optically very low. But such stagnation has been seen in other ad companies as well, like Google. This tells us that a large part of the slowdown is cyclical. The resilience of the business should suggest that once Reels gets adequately monetized and other optionalities (as discussed above) take form, we can get back to double-digit growth in 12 to 24 months.

Rising Cost

Total cost guidance for the full year 2022 came in at ~$86 Bn (74% of Sales), up from $71 Bn (62% of Sales) in 2021. Though this appears as a massive jump in absolute terms, had the growth in Sales this year been ~20% (5 yr CAGR from 2016-2021 has been 33%), Total Cost as a percent of sales would have been maintained at 62%. That being said, out of this $15Bn increase in Total Cost in 2022, Meta has already spent ~$11Bn in 9 months on Reality Labs against ~$12Bn in FY2021. Though accounting standards allow it, this expenditure is capital in nature and is not recurring. If two years down the line Meta decides to shut down Reality Labs, this will directly flow to the bottom line.

2023 Total Cost has been further increased to $96 - 100Bn. 2023 will see peaking in Opex growth as headcount growth is expected to remain flat in 2023, but the Cost of Sales would continue to rise as Depreciation expenses from capex would start trickling in.

Rising Capex

Meta is expected to spend ~$33Bn in 2022 followed by $34-39Bn in 2023. Almost all of the capex is going towards Family Of Apps, nothing towards Reality Labs. The rhetorical question is whether the scale and timing of this capex are necessary. To train the ML/AI models to better serve ads in absence of signals from 3rd party apps, it will need GPU-based Data Centers. GPUs are significantly more costly but multiple times more efficient for these ML/AI loads. Since the initial results of such an ML / AI-driven approach have shown promise, the management is certain that they would commit capital only where ROI is justifiable. This, however, does not appear to increase the Capital Intensity of the business in the long run. Meta is in an investment cycle, and it was forced to take it up given the changes in policy by Apple and soon by Google as well.

What Are We Paying For

Can FB afford to spend on reality Labs?

One of the most intrinsic and polarising questions among Meta analysts and investors is, can Meta afford to invest in Reality Labs? Though investment in the past couple of years has been very high, I doubt that Zuckerberg and the team would continue to invest in their Metaverse dream unless meaningful progress is seen. That being said, in a regular year, FOA earns an Operating profit, mostly cash, of $55-65 Bn. Spending 20% of that cash flow towards a business that could redefine computing as we know it and give the company a major platform dominance, should not be considered overspending.

Valuation

Let us understand what we are paying for the resilient part of the business.

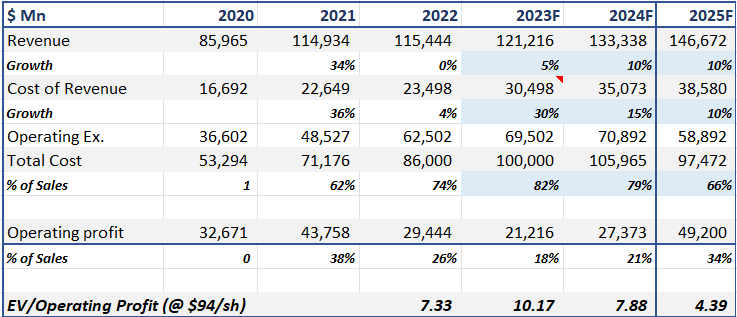

If we only look at what the resilient part of the business can deliver, aided by steps of general cyclical upturn and threat mitigation activities at Meta, the business should be able to generate an Operating profit of ~$27.3Bn in 2024. Note that all the costs associated with Reality Labs are also absorbed in it. At the current Market price of $94, we are getting the company at 7.88x EV/Operating Profit. All the optionalities and value of Reality Labs are additional.

Let us also consider a scenario where investment in Reality Labs churns out nothing, and after investing for two more years, Meta abandons Reality Labs at end of 2024.

The Operating profit for 2025 would immediately jump to ~$50Bn, absent the opex investment in Reality labs, thus bringing down the valuation to 4.39x.

Benjamin Graham said, “in the short run, the market is like a voting machine”. Maybe markets are using the share price to vote with their feet and communicate to Mark that they don’t like what he is doing. Either way, I think Meta offers a good value for the resilience and the optionality it offers, at the current price.